At the end of 2019, no one could have ever predicted what the world would look like today. The COVID-19 pandemic ripped through the world, killing millions, shutting down entire countries, and putting billions of people into financial distress. It’s unthinkable that something like this could ever happen again, but if we have learned anything from COVID-19, it should be to expect the unexpected.

While the news often cites the coronavirus’s macroeconomic impacts, what is often less discussed is the impact it has had on each person or family. Job losses, remote work, and a lack of mobility have all made this pandemic hard for everyone.

This pandemic may have affected your finances greatly, or you may have thankfully been spared. No matter your current situation, there are several things you can do to ensure you are prepared, should anything like this ever happen again. Take note of these recommendations to help keep your finances secure, no matter what happens.

The financial aftermath of COVID-19

Job losses

The first and maybe most devastating layer of COVID-related problems came in the form of job losses. It didn’t matter if you had a job for years, owned your own business, or were just starting your career—everyone was susceptible to having their jobs vanish in an instant. This is especially true if you worked in extremely hard-hit industries, like travel, hotels, and restaurants, among others. All told, the European Union had 13.7 million people unemployed in December 2020. This brought the unemployment rate within the EU to 7.5%.

While governments around the world worked to provide short-term economic relief to those struggling, this was not nearly enough to support the millions of people worldwide who had lost their jobs.

Dipping into retirement savings

For those who found themselves unemployed or having their compensation reduced, dipping into retirement savings became more common. Funds specifically earmarked for decades down the line were now used to support families during their time of need. This is a less-discussed but even more long-term negative effect of the pandemic. Using retirement savings to pay for expenses before hitting retirement age has a negative compounding effect. First, you are likely to pay a penalty for using your retirement savings early, and second, this means you will have to work harder in the future to recover the retirement funds you were forced to use.

Even if you had been prudent in saving toward retirement before the coronavirus, no one could anticipate how difficult it would be to continue paying your expenses during this trying time.

Delaying plans

If you had plans during 2020, you saw them go entirely out the window. A once in a lifetime trip? Canceled. A wedding? Postponed. What would have otherwise been reasons to celebrate suddenly became stressful nightmares, hoping that eventually, you could follow through on the previous plans you had made.

This also had a negative financial effect as well. Significant events such as these often require non-refundable deposits, meaning you might have lost significant sums of money for events that never happened. While some businesses were lenient and accommodated their customers, others were less so and may have kept your money altogether.

Financial hardship affecting mental well-being

We often don’t take into account how our financial well-being affects our mental well-being. When our world is upended, like it has been during the coronavirus, our finances are disrupted as well. In turn, we can begin to feel lonely or depressed and scared about the future. The rise in mental health issues during the pandemic has been well documented, and a major contributing factor is financial stress.

What you can do to stay prepared

We aren’t suggesting that another pandemic like COVID-19 will come along anytime soon. It’s essential to recognize the uncertainty in our daily lives and how we should always be prepared for anything because we can never predict the future. Here are a few things you can do to stay prepared if something unexpected were to happen in the future.

Diversify your income

Before the coronavirus, there was already an increase in people earning a living from multiple income sources. Side hustles from freelancing to driving for ride-sharing companies have become a regular part of working for many people. If you earn all of your income from one job, then that’s great, but it also means that you could lose your entire earning potential in one fell swoop.

According to one survey by FlexJobs, 53% of respondents said they were earning half or less than half of their income due to the COVID-19 pandemic. These respondents were likely only to have one income source, thus putting them at higher risk for uncertainty. Diversifying your income is the best way to mitigate the risk of job loss or a reduction in hours. By finding several different ways to earn your income, you spread your risk out if something were to go wrong. Let’s look at an example to show you:

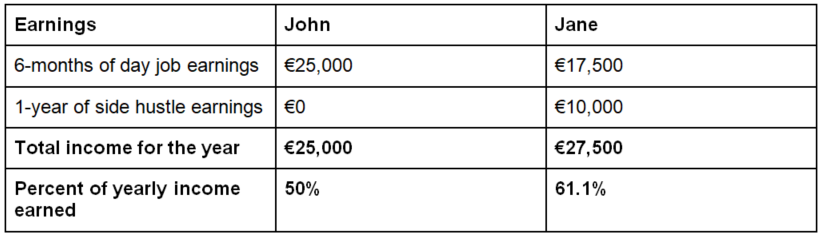

John has a regular day job, earning €50,000 per year. Jane has a day job where she earns €35,000 per year, but Jane also has a side hustle where she can pull in another €10,000 freelancing in her free time. Let’s say that both John and Jane, unfortunately, lose their jobs 6 months into the year and cannot find another job before the year ends. However, Jane is still able to keep her side hustle going through the entire year. Let’s see what their year-end earnings look like in this situation.

At the end of the year, Jane will have made more money than John while also earning more relative to her yearly income. This percentage is extremely important because we most often believe that we will earn 100% of our income each year. So, when unexpected events occur, it’s essential to have multiple income sources to keep your earnings as close to what you expected to start the year.

As you can see, when you diversify your income, you are better able to withstand unexpected twists and turns in your employment, your life, or the world-at-large.

Emergency fund

We can’t stress enough how important it is to have an emergency fund. But unfortunately, most people don’t take this seriously enough. A CNBC survey showed that 62% of people don’t have an emergency fund to pay for up to 6 months’ living expenses, 46% of respondents said their emergency savings wouldn’t last more than 3 months, and 25% wouldn’t be covered for even one month.

Your emergency fund is the first line of defense against the unexpected. It allows you to stay afloat without having to worry about day-to-day expenses or dipping into your retirement savings. This puts emergency savings at the forefront of financial protection against another earth-shattering event in the future.

Even if you already have an emergency fund, you might want to consider increasing the amount saved in this fund. If you currently have a 3 months’ salary saved away, think about increasing this to 6-months, or even 9-months if you are able. The more you have saved, the better, since you can’t predict how future events will impact your ability to earn a living.

Expect the unexpected

No, it’s unlikely that you will be able to predict the next global pandemic. But what you can take from this experience is that you never know what might happen. Next time the unexpected event might take the form of cataclysmic weather or a collapse of the housing market. Whatever may come in the future, you should keep yourself financially prepared for anything. Keeping enough emergency savings to get you through the hard times and diversifying your income to sustain yourself in difficult times are actionable ways for you to ensure your financial well-being is taken care of in the future.