KEY TAKEAWAYS

- All the countries where we currently perform lending activities (Spain, Finland, Estonia) are now profitable

- All our country-grade segments (other than 3) have produced returns in line or above the expected return

- Net yields on Bondora are highest in the marketplace lending industry

- 98% of the portfolio above target return and returns in high teens across all countries

The history of Bondora Rating

Prior to 2015

Investors invested into loans across all countries based on the data and filters that were available on Bondora. There was neither risk-based pricing nor risk estimates from Bondora – basically investors had to decide themselves which loans seemed to have a good risk-return.

January 2015

Risk-based pricing was introduced for Bondora loans a.k.a. 1st generation of Bondora Rating.

December 3rd 2015

2nd generation of Bondora Rating and risk-based pricing was introduced.

Bondora Rating helps you make better investment decisions

We introduced our credit scoring and pricing model called Bondora Rating in January 2015. In short – it’s a set of data that in combination provides a more predictable risk-adjusted return.

There are two objectives for Bondora Rating:

- We want to facilitate loans with fair prices for borrowers, considering their individual risk profiles.

- We want to deliver reasonable returns for the investors, taking into account credit risk, country risk, cost of capital and market liquidity conditions.

Overall Bondora Rating helps package all the different risk-return variables into a single number – the interest rate – making investments across different territories and segments a seamless process.

What makes Bondora Rating unique?

“Bondora Rating and unique pricing algorithm enable us to score and price loan applications from different euro area markets on like-for-like basis, taking into account both borrower risk characteristics and country risk.” Bondora Credit Modelling Team

Introduction of Bondora Rating has had a strong positive effect on returns

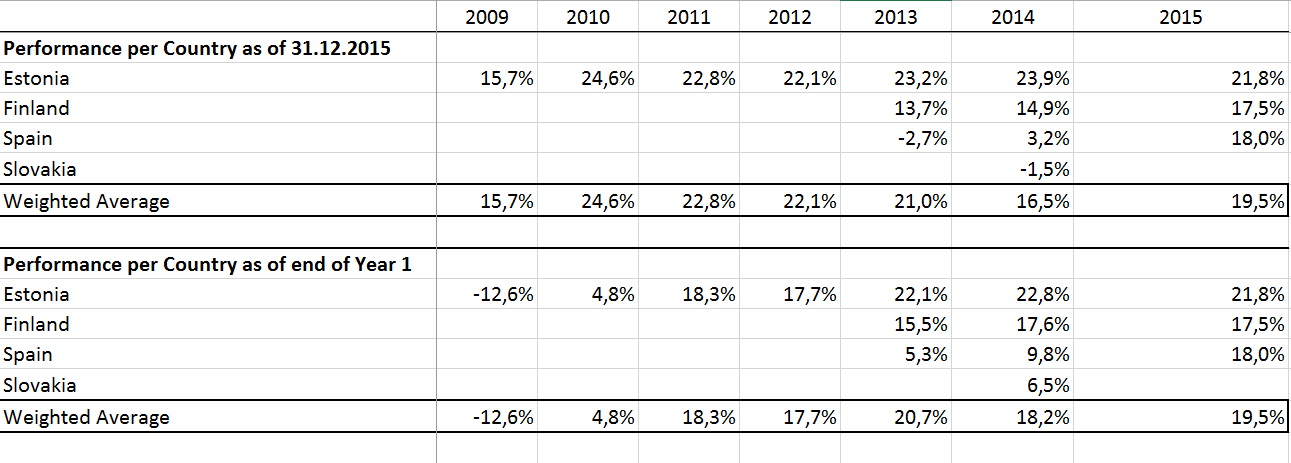

Performance by country

After Bondora Rating was implemented in 2015 the returns in new markets (Finland and Spain) have increased considerably. Spanish market that was at break-even level prior to Bondora Rating is now delivering net returns in high teens. These improvements will further strengthen Bondora’s position as one of the highest returning platforms in the marketplace lending industry (see Liberum Capital presentation page 10).

Figure 1. Performance of loan cohorts originated within the specific year as of 31.12.2015

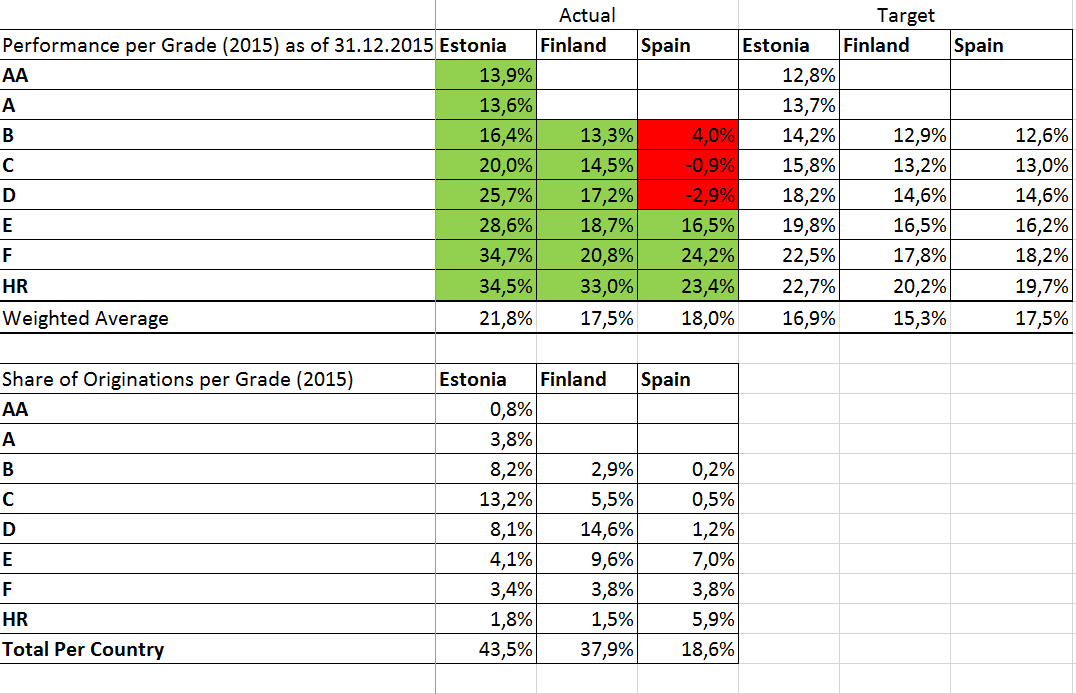

Performance by grade

Performance by grade

98.1% of the loans originated in 2015 have delivered net returns above or in-line with expectations. Only three grades performed below targets (Spanish B, C and D grades) however in total these made up 1.9% of the originations in 2015.

Figure 2. Performance of 2015 loans per country and Bondora Rating grade as of 31.12.2015

2nd generation models are built on significantly more data and hence are even more reliable

The 1st generation models delivered a significant improvement to the performance and predictability of loans originated on Bondora. However due to the relatively small sample sizes available in 2014 we witnessed performance variances between countries and grades. Therefore in order to address these limitations we released our 2nd generation models in December.

The main difference between the 1st and 2nd generation risk model is the underlying volume of historic data on which the models were built upon. The 2nd generation takes into account more parameters to estimate the probability of default of the specific customer even better.

2nd generation models for Spain and Finland were built on 10 times more data than for the 1st generation model and in Estonia we had two times more data. In effect the 2nd generation models for Spain and Finland were built on more data points than the 1st generation model in Estonia.

In addition the pricing models were adjusted to reflect changes in three other components that determine the risk-based price. Country risk factors were updated for the new macro-financial data. Risk-free rate of return was updated to reflect the current monetary conditions. Parameters of market rates of return were updated for the newly available data.

Our analysts are continuously working on finding new patterns to further improve the accuracy of the scoring and pricing systems. This is an ongoing process and remains core to what Bondora is doing.

NOW LET´S GET TECHNICAL

How are net returns calculated on Bondora?

We use the XIRR function (extended internal rate of return) to calculate the net return. XIRR is used to return the internal rate of return for a schedule of cash flows that are neither necessarily periodic (payments are not made on a single day each month) nor always positive (portfolio has both outgoing and incoming payments).

Internal rate of return is a discount rate that makes the net present value (NPV) of all cash flows (repayments minus initial investment) from a particular portfolio equal to zero. Discounting cash flow means that you are reducing the future cash flow projections to arrive at its present value (how much 100 euro in a year from now is worth today). This is mathematically done by dividing the future cash flow by 1 plus internal rate of return in the power of the fractional period (e.g. if you are using an annual internal rate of return and a payment is 4 months from now then you would take 1 plus internal rate of return to the power of 4/12).

XIRR uses the loan issue date and amount, loan actual repayment dates and amounts and sum of scheduled future principal repayments (this is assumed by us to equal the present value of the portfolio) to calculate the internal rate of return of your investment portfolio on Bondora. This approach writes off all overdue and unpaid principal and interest payments immediately from the calculation. No assumptions for future interest payments or loss provisions are made as this is expected to be covered within our approach to arriving at the present value of the portfolio.

In other words, if you would borrow money at a rate equal to the net return shown on Bondora in order to finance your investments you would end up break-even. If you are borrowing money at a lower rate or your alternative investment opportunities (e.g. mutual fund) have a lower rate of return than you are making a profit compared to other options and it makes sense to continue or increase investment.

Can net returns of an outstanding portfolio change over time?

Yes, your net return over time can fluctuate based on the actual interest and principal repayments received. Overdue loans might start performing again and current ones become delayed. Recovery processes can take years to collect every penny owed, so even performance of very old portfolios might increase substantially over the years. Over time our servicing, collection and recovery practices are continuously improved and even higher risk portfolios can start behaving like lower risk ones.

Most of the fluctuations (calculated as the current net return vs. the net return calculated in the end of the specific calendar year) we have witnessed have been positive due to recovery efforts. Using data since 2012 there have been variances between -8.1% to +4.4%.

Figure 3. Performance per country

Can the net return calculation be improved?

Theoretically it would be possible to substitute the current present value sum of scheduled future principal repayments with the sum of actual discounted future cash-flows. However in order to accomplish this you would need to make a significant amount of assumptions about the timing and amount of the future cash flows from your outstanding portfolio. You would need to estimate when and how much would current loans repay and you would have to make the same assumption also for delinquent loans. Furthermore, you would need to discount these cash flows with a rate equal to actual XIRR of the fully matured investment or use future dates and payment amounts granularly in the model . In the end, one would simply arrive at a number based on a lot of assumptions that still needs to be tested in reality.

We have seen some investors build their own risk-adjusted models that simply take the outstanding principal balance and reduce this by a fraction of the overdue loans. Although this might at face-value seem like a reasonable step, it ignores the fact that outstanding loans will make both interest and principal repayments, as will recovered loans. This logic could be applied to investments with very low rates of return (where future interest payments are discounted to zero or to negative numbers) however not to consumer loans carrying reasonable risk-adjusted interest rates. In other words in case one would discount overdue loans at the same time performing loans would be taken into the present value with a premium.

In case you are interested in trying to establish a better model for calculating the present value then we recommend using the Historic payments and Future cash flows data exports under public or your personal data. Simply using outstanding amounts is not sufficient for building a model.

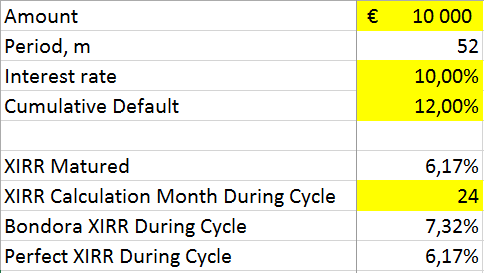

The enclosed file gives you a template example of discounting future cash flows and calculating XIRR at different points in time over the cycle of a portfolio. It also includes all the data used in the actual return calculations presented in the analyses above. Sheet ‘Xirr Calculator Example’ displays a basic model that includes some elements to include in your own analyses. Cells in yellow can be edited and white cells are fixed (please note that this example is for a 52 month term portfolio). Calculations related to ‘Bondora XIRR’ are based on the logic currently used on Bondora whilst ‘Perfect XIRR’ calculations are based on a situation where one would have perfect information available at any time during the cycle.

Figure 4. Bondora XIRR calculation model

Can net returns be positive even in case default rate is above the interest rate?

Net returns on a portfolio can be substantial even if cumulative default rate is equal or even above the nominal interest rate. This is because the performing portfolio continues to generate interest and repayments over the full cycle of the loan not only in a single year.

Over an average 52 month cycle the performing loans and parts of the non-performing loans generate and pay interest for 52 months. Therefore in case one would want to compare this number with the cumulative default rate then the nominal rate should either be cumulated as well or the default rate annualized over the 52 month period. In the calculation model shared above we have built cash flows for an imaginative portfolio with 10% nominal interest rate and a 12% cumulative default rate to illustrate this.

We have seen some investors build analyses where portfolio returns have been calculated as interest rate less cumulative default rate (or cumulative expected loss). Furthermore some of these analysis have been done by calculating tax income on the nominal interest rate although non-performing loans do not pay interest and hence are not taxed. Such models unfortunately are misleading at best due to the reasons explained above.

Please make sure you use the full cash flows when building your own portfolio evaluation models and apply taxation only to actual paid interest not nominal values.

*Correction: Amount lent per country figures were updated in the enclosed file to use the same definition for an issued loan as in the cash flow calculations, share of originations per grade and general statistics on Bondora website. This change slightly affected Weighted Average results, most notably net return of 2013 originations decreased by 0.1 per cent to 21.0% and net return for 2014 originations increased by 0.4 per cent to 16.5%.

Thank you for post that makes ground for discussion.

Few questions:

I am right that Performance in this post mean XIRR?

What you name defaulted – is it basically loan with AD=1 in loan dataset or something else?

It is a bit unclear for me, if 36month loan started overdue after 4 month of payments, to calculate XIRR you will use only 4 payments or you will count 4 payments plus some future payments?

One more question. you said “Net yields on Bondora are highest in the marketplace lending industry”. What is compared?

Last observation. When you said “Performance of Slovakia” just -1.5% (Figure 1), it destroy trust in all you said. Argument please.

Andrej, thanks for questions. I’ll start from the back.

Firstly all calculations are enclosed in the file referenced in the post – https://www.dropbox.com/s/fhi88j0v222a4mb/Xirr%20calculations%20as%20of%2031.12.15.xlsx?dl=0 The file includes all the data and formula used to calculate the performance. You can see the actual cash flow of Slovak loans from this file as well as the calculated present value used in the XIRR formula. The methodology is explained under “NOW LET´S GET TECHNICAL” section in detail. In case you have other thoughts then please let us know what specifically needs to be changed.

Secondly, Liberum has conducted a study to compare the performance of the portfolios on different marketplaces. The relevant section is titled “Platform net yields swapped into USD (expected seasoned returns)” where they have a) looked at cash flows of seasoned loans and b) accounted for currency fluctuations in order to make the performance relevant to US investors. The link is enclosed within the text – https://s3-us-west-2.amazonaws.com/lendit/europe/2015/presentations/day1/pdf/Cormac+Leech+Presentation+PDF.pdf

Thirdly, performance and net yields in this post are calculated using XIRR function in the way explained within the section “NOW LET´S GET TECHNICAL”.

Fourthly, our credit models aim to predict the annualized defaults. Loans with AD = 1 in the dataset are part of the dependant variables that we are trying to predict.

Finally, the examples can be modelled using the template we have provided in the text. However in a the following scenario where: a) a loan has 36 payments in total; b) it made 4 payments in full; c) then over the next 12 months it made let’s say payments in the value of 4 payments; and d) the calculation is done before month 19 then the XIRR function would have positive cash flow in the respective dates and amounts the 8 payments (4 on time and 4 partial/recovered payments) were made and for present value use the sum of planned principal payments for payments 19 to 36.

Hope this helps!

Partel, thank you , I have not noticed file at the beginning.

My personal opinion – if I understood right, I cannot agree that performance as you told in example is right and correct. You count all scammers who repaid 1 or zero payments as “good”. I mean Spanish Scammer took loan for 36 month and not paid at first month. Now is month 2. You are telling that to calculate performance you will skip month 1 and count 35 month as “good”. This is definitely too optimistic.

Overall, I am 100% sure that any investor, as well as Bondora, will not buy i.e. my portfolio (I am in top 10-15 of investors) for 90% of what you name “Account value”.

Andrej, section called “Can the net return calculation be improved?” lists alternative mathematically sound options to calculate the present value of the portfolio. Our approach is one of the alternatives and over the past years there is no proof that it is optimistic or pessimistic over the cycle. In case you have alternative approaches then please test these out with the data available and highlight specific approaches that are more precise for modelling the future cash flows of a portfolio.

PS! Regardless if there is a liquid market for trading your portfolio the calcualtion of present value based on future cash flow would not change. This would only change the yield calculation in case you would use the market value of the portfolio in the evaluation.

Is this serious?

I mean… you are validating the quality of your rating by using the implicit assumption that the rating is correct on the biggest part of the actual data?

I wonder how with this fudge you still managed to get these Spanish credits into the red, the actual losses must have been dramatic.

Can we somewhere get the raw data on overdues for 30, 60 and 180 days?

This is no way to generate trust.

Hi Jörg, all of our data has been publicly and daily available under the Data Export sections in the public as well as the investor personal web for more than 2 years. Please take a look. There you can download all the future and previous cash flows as well as hundreds of data points on the existing loans.

Please note that a default is not an indicator of a loss or write-off but a signal that the loan is being serviced through collection and recovery processes, rather than through ordinary processes.

XIRR may be a good calculation to compare different investments for the past but it doesn’t give a good and fair summary value in case of parts of portfolio goes to default.

Explanation:

– in the first time you get interests for the most loans. Interest parts are very hight and repaiment of pincipal is low. So even if a great part of loans default there will be a great positive XIRR.

– later even the loans paying in time pay fewer and fewer intersts. The principal part grows up. So your XIRR will go down dramaticly.

I invest since 2008 in p2p. Allways if you stop to bring fresh money in your investments, XIRR goes down by system.

So you need a second indicator to look up for the future. I don’t say that XIRR is wrong but it isn’t the whole story and it must go down over the years.

Hi Martin, in the section “Can the net return calculation be improved?” we highlight alternative options for calculating the present value of the portfolio. The data on the portfolios is fully available under the public and private data sets so it is possible to build custom models if you want to use different assumptions for future payments.

I do so. But most of your investors don’t.

On the one hand you tell us that must of the costumers aren’t able to set a few option on portfoliomanager on the other hand they should handle complex data analysis to recognice how their portfolio may perform until the end of its lifetime? Be serious. Be fair. Tell the whole story. Investing at bondora is risky. Thats not the point and 10% or more profit a year is nothing anybody can blame you. But showing XIRR rates of 20% or more is missleading.

Investors have the option to use the investment tools and reports available on Bondora or build their own ones using the data exports and API. The way net returns and present value is calculated has been in place since 2011 and there has been no grounds or reasonable alternatives so far to change it. However active investors interested in complex models can use the data we have uniquely made fully available to build alternative reports.

Investing in general carries risks. Higher potential variability in returns is in general associated with higher risk regardless of the asset class. Therefore investors can earn a premium to compensate for the potential added risk.

Taavi tried to calculate what you say “Can the net return calculation be improved?” method. It was very fast said by Bondora that he is misleading.

Presented method of calculation when Bondora counting scammers as good payers is, in my opinion, fairytell. I am worry if Bondora leave in that “fairy” virtual reality. Sorry. Bad. Not fair especially for not professional investors.

Almost all modelling attempts shared publicly by commentators have fallen on the fundamental errors described in the third paragraph of the section “Can net returns be positive even in case default rate is above the interest rate?”. Such results are misleading as the calculations are not correctly executed.

In a recent past in an interview Partel said that new ways to calculate the fair value of the portfolio would be implemented in last november or december. And even though they didn’t do it, his team said it was schedule to be implemented in the first quarter of 2015.

Now, after reading this I can only think that those plans were canceled. I don’t like conspiracy theories, but the reason for this seems clear for me. Trying to get new investors to join in by hiding the real statistics.

As for closing the forum, I just have to say, many of the people commenting there are in the top 20% of the people with the most money invested. And if they happen to run blogs and influence people, it should be no reason to shut them up.

We are rolling out an alternative way to model the value of the portfolio very soon. Investors will then be able to use their own assumptions for modelling future cash flow for the calculation of portfolio value.

All of our data has been publicly available for nearly 2 years. These datasets have only been extended over time, not reduced. We are the only marketplace with such granular data available publicly as well as for each specific account.

We have found a partner to take over the forum so that the active community would have an online channel for communication. This simply will not be hosted under our site and will be in an environment where investors from many other platforms are all together. In terms of numbers, forum users funded 3.27% of the investments over the past 180 days.

I have a few question regarding the “Performance by grade”.

According to the official statistics, the Expected Return for grade F is 15.86% and HR loans are expected to return 14.36% (as of today). Just 9 days ago (28th of december) the expected returns were F = 16.32% and HR = 15.32%. That means HR loans expects to perform a full percentage less in just 9 days? That makes me wonder what the numbers will look like 3 months from now. Can you explain why the numbers change so fast? I thought those expectations were based on years of historical data? Did you wipe all historical data and only use the new 2nd generation Performance grading for the expectations?

In Figure 2 the Actual Weighted Averages of F and HR loans are 20,8% to 34,8% in all countries. If the actual return is so high, why are the expectations of the future only 14%-15%?

Expected Return chart is based on latest data (30 days) from the marketplace to reflect the current market situation. Portfolio profitability, recovery rate, the charts in the Returns and General sections are based on full set of historical data.

The actual returns are below expected returns as we have not witnessed any ‘unexpected losses’. Unexpected losses (UL) are losses above expected levels (i.e. above EL) that are expected in future but cannot be predicted in terms of timing or severity. We account for such events to occur and for higher risk loans the actual returns will be considerably higher than estimated ones due to very high risk buffers.

In statistical terms, unexpected loss (UL) is often defined as standard deviation of the expected loss (EL). However, portfolio loan losses are not normally distributed. Instead, the small losses around or slightly below the expected loss occur more frequently than larger losses. At the same time, the distribution is fat-tailed meaning that rare severe losses are more frequent than normal distribution of events would allow to assume. Therefore, UL is defined as the loss exceeding the EL at the chosen confidence level, assuming fat-tailed distribution.

One important feature of the UL curve, s that it reverses at around default level 35-40%. The logic is that while expected loss increases, there is less room for unexpected losses. From the perspective of investor returns, this feature means that from certain EL level onwards, expected return for covering unexpected loss part starts declining; accordingly, relative importance of the expected loss component in the investor interest rate increases.

Therefore HR loans can at times have lower estimated returns than F loans as our pricing model has added lower additional buffers for UL into the pricing as the expected loss buffers are already considerable. In case long-tail events do not occur, the performance of HR portfolios is expected to be higher, but in case of long-tail events occuring and in case they impact higher risk loans more than lower risk loans (as assumed by our models) then the actual returns would be lower than for F grade.

Long text, but I hope it answered your question.

You explain that high default rates are compensated by long payed interests. That may be right for longer terms (even if a lot of borrowers fail to pay the first rate).

But can you explain the calculation for the following spanish loan:

Amount: 1595€ Term: 3

Interest: 48.84%

Probability Of Default: 50.8%

Expected ROI: 14.77%

Loss p.a.: 34.07%

https://www.bondora.ee/en/Auction/Show/7ae2b2d7-d326-4b85-9107-a57e00cfa09d

The borower won’t pay a lot of interests IF he will pay anything at all. Can’t see a 14.77% ROI.

You should read it as follows: a portfolio of such loans (minimum 200 loans to have a fully diversified portfolio) would expect a 50.8% default rate over a 12 month period. During this period the defaults increase periodically with a certain curve until they reach the estimated level by end of the year. A cohort of such shorter term loans would not be expected do reach these levels even before any recoveries.

We are showing annualized numbers instead of cohort based numbers as our pricing model assumes that the investor keeps the portfolio fully invested (interest earning balance remains does not decline).

In a portfolio that continously invests in the highlighted 3 month loans we would expect to see the expected defaults as it assumes that repayments are invested in new loans and hence over time the default builds up (as defaults from multiple cohorts accumulate).

Thank you, that helps to understand. I did similar calculations (for longer terms only) and came to similar conclusions: default rate higher than interest rate on a rich spread portfolio can generate good wins in the end even without recoveries.

But I am not so optimistic on short term loans. The repayment is very high for the borrower and the profit in absolute numbers isn’t high at all, the risk it’s not scaled down as much as the term is.

It’s a very good idea that you give us answers to our questions. I guess people have to learn to accept high defaults on high interests and they will only do it if they understand that there stay very positive returns anyway. So if you build some more examples this will help more than hide defaults in the statistic view of the dashboard.

Thanks for the kind feedback Martin!

The main question here is though:

a) Why would you compare XIRR calculation to Bondora Rating’s Expected Return?

b) How would that say anything about the performance or accuracy of Bondora Rating’s predictions?

They are two different beasts.

XIRR function is used to calculate the actual return of the portfolio. Expected Return is used to estimate the return of the portfolio prior to the investment.

I understand what XIRR does and shows.

The question is, how can you say anything about the accuracy or performance of Bondora Rating, by comparing XIRR to the Expected Return figures?

And why would you compare those two in the first place?

Investors use Bondora as any other investment product to achieve a certain return on their portfolio. The expected return shown to investors prior to the investment gives an indication of the potential net return of the investment whilst the actual net return gives the investor the actual performance of their portfolio. Net returns are the only comparable metrics between different asset classes and portfolios. All other metrics are simply parameters used to achieve or estimate a net return.

I agree, you can use net return to compare your returns with other investors/portfolios or different investments. Of course, first you would adjust/modify the calculations to make sure they are using similar/matching calculation logic to be able to compare them. Otherwise you could easily end up comparing two random numbers. Which is often the case with many of the P2P-lending platforms for example, because they often use different calculation logic.

However, my question actually is, how can you say anything about Bondora Rating’s accuracy or performance based on this XIRR calculation?

I would like to close this thread by reiterating what I said above. Both actual net return and expected return use the expected cash flows to calculate the internal rate of return for the portfolio. Actual net return is based on actual data combined with a projection for future cash flow and expected return is entirely based on a projection and assumptions for the cash flow curve.

Bondora is not a credit rating agency nor provides rating services. Therefore we do not market the accuracy of the parameters used in pricing loans but the end result – the net return. The article above does not make any statements about accuracy of the predictions. The article discusses what Bondora Rating (credit risk scoring and pricing model collectively) has achieved in a year by increasing the net returns across all markets and delivering strong positive returns, above expectations in many cases.

Partel I see from your results that the average loss for the Slovakian loan experiment in 2014 is 1.5% based on your chosen method of measuring profit.

I find it very hard to believe that this gives a true profit value when I look at the 36 loans I have made to Slovakians. Of those 30 have defaulted with almost no recovery, 2 are late and only 4 are making normal repayments.

Can you really convince me that my loss from these loans will eventually only be 1.5% or thereabouts and that the Bondora profit shown to investors is based on reality rather than wishful thinking?

James, the methodology used for measuring profitability has been used since 2011 and you can see the actual results and the variability in the charts above. This methodology is not based on wishful thinking but the assumptions presented in the article. Specifically about Slovakia then the data enclosed within the article shows that Slovak portfolio generated cash flow of 96,000 euro. Loans in default have been serviced by a debt collection agency and a new firm is added even this month. The servicing of this portfolio is an on-going process.

I don’t understand it too but the numbers here are similar:

https://peerlan.com/?countries%5B%5D=SK&breakdowns%5B%5D=countries&breakdowns%5B%5D=loanDates&breakdowns%5B%5D=purposes&breakdowns%5B%5D=ratings&loanDateRange%5Bstart%5D=2014-01-01

So let’s hope for better recovery now.

I want rather to ask about the debt collection. When you switched to the new debt collection model Bondora said that each DCA will get 3 months to show results. Now I see many loans, however, where one DCA has finished processing after 3 months without any success usually somewhere in the early December, however, no second DCA has been assigned to the loan so far. There are also some loans that are still assigned to the same DCA for more than 3 months without any repayment in this timeframe. I sometimes also encounter loans that defaulted quite long ago (up to a year), but there seem to be no debt collection actions whatsoever (neither DCA nor court cases). Can you please explain what is going on in all these scenarios. I think you will agree that it is very important to launch the debt collection as soon as possible and also to submit the legal claim at the earliest possible moment, because it is quite likely that other parties will also want the piece of the debtor and it is very important to be among the first with the claim. Please comment.

Denis, all DCAs completed the minimum 3 month period only just now as some took longer than expected to get fully operational. We are now evaluating the performance of each of the partners to decide which partners will be kept and if any new ones will be added to the mix. Thereafter the non performing portfolios will either be transferred between DCAs, kept with the good performing ones or legal action filed.

In 2016 we are looking to further optimize the external collection process and start actions as early as possible. All old cases are being reviewed meticulously to ensure that everything has been processed in the best possible way. In case you have any specific examples please shoot me an email with the links ([email protected]) and I’ll pass these to our C&R team to verify the status.

I strongly doubt, that the reported figures show any resemblance to the real situation. Judging from my experience at Bondora, defaulted loans get rescheduled just to default again over and over. Sure, this way you can show an astonishing ROI. And mathematically this is even correct.

The thing is: It just completely ignores reality.

Let’s have a look at my account:

Most of the loans in my portfolio have defaulted at least once and have been rescheduled, sometimes several times. Still, right now, most of my loans show missed payments (again). Yet Bondora calculates a stunning 21.13% Net Return for my portfolio!

The statistics tab also tells me, I’m amongst the top 40% of lendors. I feel very sorry for the other 60%. No, actually I feel very sorry for ALL lendors, because Bondoras profit claims are a dishonest disgrace.

Daniel, if we put assumptions aside then only 3.68% of loans in default have been in this status twice. Furthermore if a loan does not make payments then the ROI is immediately reduced regardless if a new payment plan has been agreed or not. Therefore the claims you make are not correct. When evaluating the performance of a portfolio one needs to look at the cash flows (including what has been the net investment into the portfolio) as explained in the article above not simply the loan status split.

Pärtel,

I cannot check the validity of your claims about statistical figures regarding the whole bondora loan portfoio.

But I made the effort to calculate some statistics for my personal bondora portfolio.

On 12.01.2016 bondoras statistics tab tells me my net profit is 21,11%.

Now, my portfolio currently consists of 103 loans. So there should be at least SOME statistical significance.

The loans are spread as follows (all percentages are calculated based on the principal amount of the loans):

AA 3,5%

A 7,0%

B 12,7%

C 33,1%

D 19,0%

E 4,2%

F 6,2%

HR 14,5%

Average Interest: 27,3%

(Additional Info: I also traded a very small number of loans on the secondary market, but without calling or paying significant bonuses. So there shouldn’t be a big effect on the profit caused by those trades.)

Note: The following percentages are ALWAYS based on the total principl value of the portfolio.

Now, the first thing that strikes me, is that 41,8% of my loans have been rescheduled!

Roughly half of those (19,8% to be precise) have then defaulted again and are in collection process right now!

In total, 39,5% of the loans of my portfolio are defaulted and currently in collection process! The collection process has recovered 6,4% of the principal. So theres currently an expected loss of 33,1% of the principal to defaulted loans.

Additional 15,2% of the loans in my portfolio show delayed payments.

Now, with those statistical figures, are you really trying to tell me, that the current net profit calculated as 21.11% shows a realistic picture?!?

And if the same formulas are used to calculate your profit figures reported for the whole bondora portfolio: How realistic are those figures then???

Hi Daniel, thanks for the detailed question. Firstly I would like to note that loan rescheduling should not be taken as negative sign. This is a standard option convenience option provided with consumer loans to help borrowers adjust to any changes in their finances that might occur over the term of the loan.

Specifically I emailed you an overview file that demonstrates the way we would analyse the performance of your portfolio through the cash flows. I unfortunately cannot share the results in this blog but I can assure the public that the calculations on the full portfolio future cash flows that include loss provisions confirm the current expected portfolio return.

As stated above, it’s not the math, but the method/ formula I doub’t to draw a realistic picture of the net returns to be expected.

In the end we will have to conclude this discussion with the statement: We agree to disagree!

Thanks Daniel for the feedback.

As we discussed over email I agree that there can be many ways at looking at the future and I listed different alternatives in my article. There can certainly be other alternatives used by investors and this choice is open to every single person. It will be impossible to get everyone to agree on the same assumptions on the future or to agree that somehow one’s view is better than another person’s assumptions. Some people are always pessimistic, some optimistic.

In the coming two weeks we will release a new tool allowing investors to use different discount values to make deductions from their future expected cash flow depending on the status of the loan. This will provide you and others who have their own conviction of looking at the future a simple way to calculate alternative values for their portfolio using their preferred approach.

I hope you will like the tool!