In October we launched our new dashboard and Portfolio Manager. Since then we have polished the interface according to your feedback and we are happy to reveal two improvements.

Upgraded design of the Portfolio Manager

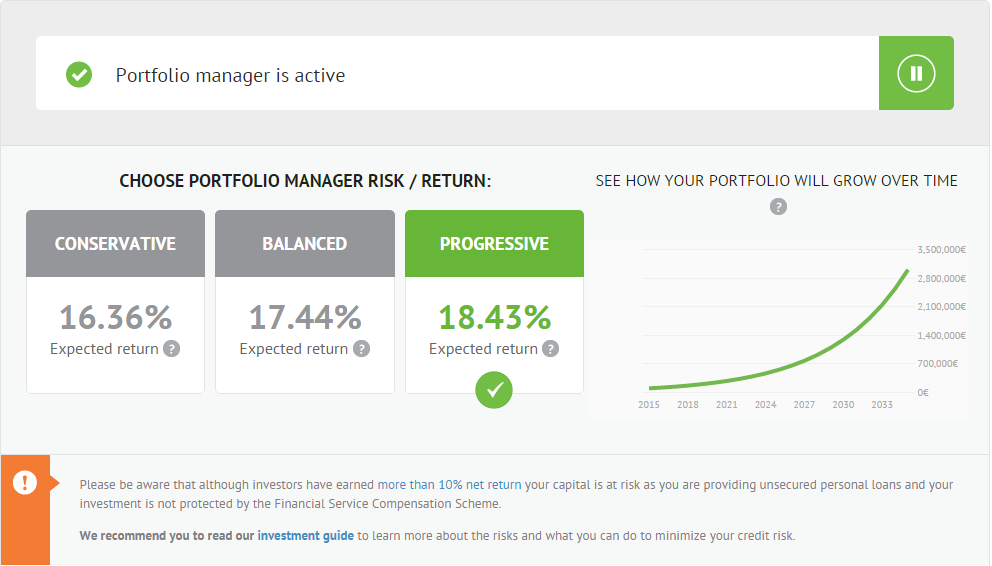

We have replaced the slider with three separate sections of the risk-return choices. The design is much more convenient now – moving from left to right you can change your risk-return level and see your expected return change accordingly on the graph.

We have replaced the slider with three separate sections of the risk-return choices. The design is much more convenient now – moving from left to right you can change your risk-return level and see your expected return change accordingly on the graph.

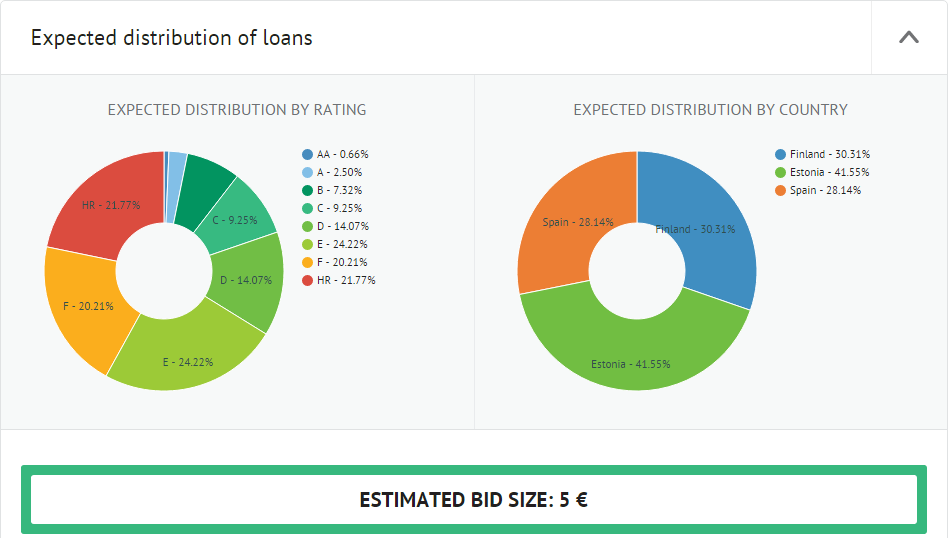

Power of automatic diversification – estimated bid size is added to the dashboard

Regarding the new Portfolio Manager these are the frequently asked questions from our support team:

What is my current bid size and how is it determined?

Our technology adjusts the size of each investment amount based on the number of unique borrowers in your portfolio. The system carefully increases the investment size as your active portfolio grows while making sure the risks do not increase. The investment size can also be adjusted downwards if the size of your portfolio starts decreasing.

The minimum bid size is 5 euro and maximum 80 euro. The bid size is doubled after each time your portfolio increases by 200 loans. 200 is an important number because analysis of the investors’ portfolios shows that the risks of a portfolio substantially decrease after reaching 200 unique loans. This means that your portfolio return becomes stable and on 95% of cases is above 10% of return. Therefore increasing the size of the investments after each 200 new loans allows you to lend your money faster without increasing risks.

Why is my Portfolio Manager not investing even though I have available funds?

There can be two reasons for that:

- If your available balance is less than your current bid size, the Portfolio Manager waits until your available balance reaches your bid size.

- Check if your Portfolio Manager is activated properly to make sure it has started investing.

To sum up, the estimated bid size has been a requested feature for the new Portfolio Manager and it is going live with our release this week. We hope this makes your experience with Bondora even better.