Cash, and more so the lack of it, can be a determining factor in whether you will achieve your goal of financial freedom. In short, cash flow is the net amount of cash that is flowing in and out of your accounts each month. Traditionally, this has been an important measure for business owners as they can keep track of how much money they are generating from customers that they offer their services to. It’s also important for them to know how much they are paying out each month for things like business loans, office rental and many other expenses.

However, the same cash flow measures can be used by individuals like you and me. Let’s say that each month you earn €2,000 net per month from your employment, €500 from your side hustle and €200 from your investments. But you need to live, so you can deduct your mortgage payments, car costs and any other expenses you have. The result of this will be either a positive or negative cash flow.

Cash Flow from P2P, Real Estate and Income vs Accumulation Funds

One of the most popular asset classes today is Peer-to-Peer lending, notably for the opportunities it gives investors to become the bank and receive a monthly cash flow. Let’s say you invested €10,000 across thousands of loans from a range of risk ratings, loan durations and countries. Every month, the borrowers will make their loan repayments which consists of principal and interest, you then have the option to withdraw this cash flow or reinvest your profits to compound your interest and maximize your overall returns.

Quite similarly, real estate investments work in a comparable fashion. If you buy a rental property for €100,000, each month you will receive a payment from the tenants (e.g. €600 per month). You might use some of that to pay the remaining mortgage on the property or add it to a growth account to save a deposit for another property. An important difference between this and P2P is risk, as previously mentioned you can spread your risks across thousands of loans where as you rely on the payment from a tenant in a single property – if they default then there is no other cash flow. Protect your cash flow by diversifying within your chosen asset class.

If you are familiar with investing in equity funds, it’s likely you have come across the accumulation vs income conundrum. Simply put, an accumulation class fund will reinvest any cash generated from the investments within back in to the fund, over time this can significantly increase the size of your total pot. On the other hand, an income class fund will pay any cash generated from the investments back to you to use as you wish. This is for those who are looking to increase their total monthly cash flow amount and are not necessarily focused on the long-term growth of their investments. Almost always, the accumulation fund will be the most profitable in the long run.

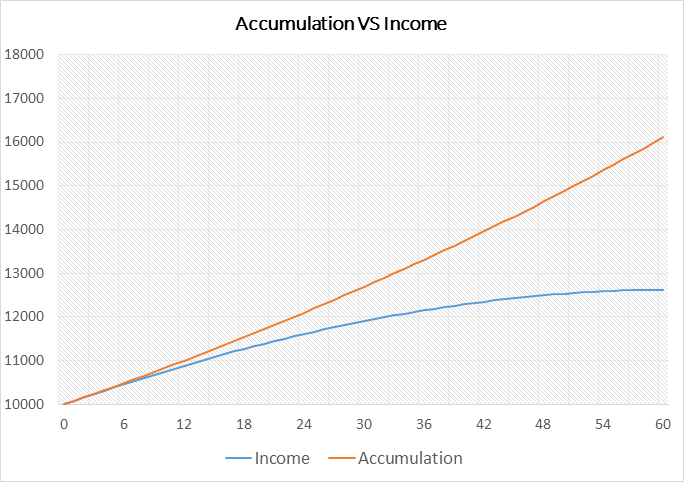

Take a look at the graph below:

The same principle can be applied to your investments with Bondora, as the only difference is the underlying asset (consumer loans rather than equities). In the graph above, we have compared the growth of a portfolio with the same interest rate, starting capital and duration, the only difference being reinvesting your monthly cash flow compared to withdrawing it each month. Using our Portfolio Manager, starting with €10,000, an outlook of 5 years and a respectable interest rate of 10% per annum, there’s a stark differential in performance.

In fact, by simply allowing the Portfolio Manager to reinvest your monthly cash flow, your account value at the end of the 5 year duration would be 33.9%, or €4,462 larger (€17,623.42) than if you did not (€13,161.42). This is literally how you can “Make your money work for you” with minimal effort.

Cash for thought

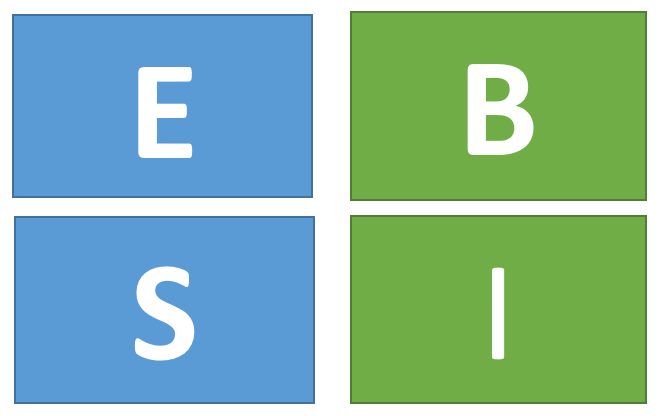

Do you recognize the quadrant above? If you do then you are most likely well accustomed to the benefits of having a positive cash flow, congrats! For those who are still puzzled, this peculiar yet simple diagram is the brainchild of Robert Kiyosaki, the king of cash flow. As the creator of the Cash Flow Quadrant, Kiyosaki divides the general population and their mindset in to 4 separate categories:

- E: Employee – This person values job safety and security over everything.

- S: Small business owner/Self-employed – An independent person who wants to do everything related to their business by themselves.

- B: Big business owners – People who create a large business run by intelligent people.

- I: Investor – Those who make money work for them.

His main theory is that people should learn how to become big business owners and learn how to become investors, as the people on the left side of the quadrant only have active income compared to those on the right earning passive income. Creating a viable and sustainable source of passive income is seen as a core principle of achieving financial freedom. Read more about this here.

What are your favourite books on investing and cash flow? Leave us a comment below and let us know.