Euribor, or Euro Interbank Offered Rate, is the average interest rate a group of European banks charges other banks to borrow money. Euribor rates are used as an index or reference rate across financial industries that use the euro, impacting everything from savings accounts and home and car loans to more complex derivatives trading instruments.

Which banks make up Euribor?

Euribor was first introduced in late 1999, offering a more universal reference rate for Europe. Before 1999, individual European countries had their reference rates. The panel of European banks that comprise Euribor are those that conduct the most business, measured by volume. Some members include BNP Paribas, HSBC France, Deutsche Bank, Banco Santander, and Barclays Capital.

What determines the Euribor rate?

The Euribor rates are determined by supply and demand, the broader economy, and the inflation rate. When the central bank discusses plans to hike or slash rates, Euribor rates are also indicators of future interest rates, rising and falling.

When more people want to borrow money, the Euribor rate – like interest rates – increases. Today, there are five Euribor rates, each reflecting different loan term lengths, from one week to 12 months. The 12-month Euribor rate is often considered the most relevant to consumers because banks rely on it for setting their mortgage rates.

History of Euribor rates

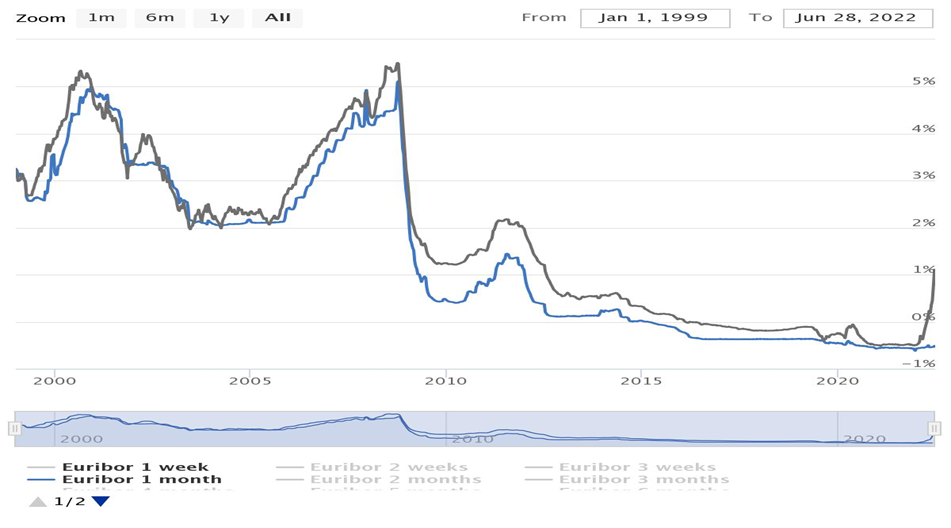

When Euribor rates were first published in 1999, the 12-month rate was around 3.2%. As interest rates rose in 2000, so did Euribor rates, until they dropped sharply in the aftermath of the September 11 attacks. For three years, from September 2005 until September 2008, rates climbed steadily, culminating in Euribor’s all-time 12-month high in early October 2008.

The subprime mortgage crisis and the housing bubble burst in the United States sent shockwaves worldwide. Euribor rates nosedived in response, plummeting from 5.5% to 1.2% in less than a year as governments and banks desperately tried to stop the bleeding and prevent a full-blown recession.

When the global economy began to recover in 2010 and 2011, Euribor rates ticked up, until 2011 saw a drop that led Euribor rates down to all-time lows of less than 1%. Rates continued to fall until, in early 2016, Euribor’s 12-month rates crossed into negative territory, where they stayed at historic lows for more than five years.

What’s happening with Euribor rates in 2022?

Euribor rates started 2022 in a similar fashion to the previous several years. However, the days of ultra-low rates appear to be behind us, with rates soaring in Q2 and Q3, breaking the 1% barrier for the 12-month Euribor reference.

After the European Central Bank (ECB) announced it would increase rates for the first time in over a decade, Euribor rates spiked, as expected. Spurred by the armed conflict between Russia and Ukraine, global supply shortages, and lingering COVID-19 shutdowns, the ECB and other central banks are scrambling to raise rates to fight record inflation. Euribor rates took off like a rocketship in just a few short months, increasing severalfold.

After an extended period of below-zero rates, Euribor shot up in 1H 2022, breaking 1% for the first time in over five years

While no one can be certain, Euribor rates appear to continue their ascent as the ECB hikes rates. There is, however, the possibility that the ECB dials down its fight against inflation to avoid a recession. Still, inflation seems to be the priority right now, so Euribor rates will likely move higher.

How does Euribor impact your daily life?

You might think that rising Euribor rates don’t have much of an impact on your daily life or finances, but that couldn’t be further from the truth. Euribor rates are sometimes called “the price of money” because they represent how much it costs to borrow money.

Euribor can affect you directly by increasing or lowering the rates on your savings accounts and any variable-rate loans you might have, such as your mortgage. If you have a variable-rate mortgage and the Euribor rate continues rising, your mortgage payments will increase. Alternatively, if the Euribor rate happens to decrease, you can expect your variable mortgage rate to go down, too.

Rising Euribor rates indicate that money is more expensive to borrow, so people and businesses are less likely to make unnecessary purchases. This tends to reduce inflation, but comes at the cost of slower economic growth. Businesses that borrow money have to spend more, which can result in increased costs that are often passed to consumers like you. At some point, you’ll decide these higher prices aren’t worth it, and you’ll refrain from buying. When enough consumers have that same feeling, demand will decrease, slowing inflation and the economy.

Euribor rates can also translate to employers offering lower wages, slowing hiring, or even cutting jobs. If a company has to pay more to borrow, it will usually think more carefully about how essential it is to take that loan. Every euro will start to matter, particularly when consumer demand decreases.

You can think of Euribor rates as interest rates, since they both affect the price of money and how much it costs to take out a loan. Euribor rates are constantly moving to try and balance economic growth and inflation.

When Euribor rates are low, borrowing money is cheaper; when rates are high, the cost of additional interest makes everything more expensive. If you have a variable loan or are planning on taking a loan of any kind in the near future, Euribor rates are especially relevant to you. The truth is, Euribor rates impact every sector in the economy (and the economy itself), even if you don’t necessarily feel the change in your daily life. So, if you care about money or the economy, you’ll care about the Euribor rate.