Recently, we’ve released several posts that explore the origination of loans by unique data like home ownership, education, employment duration and more. This month, we’re going to do the same and compare how this has changed in comparison to the previous months.

Average income, loan amount and age

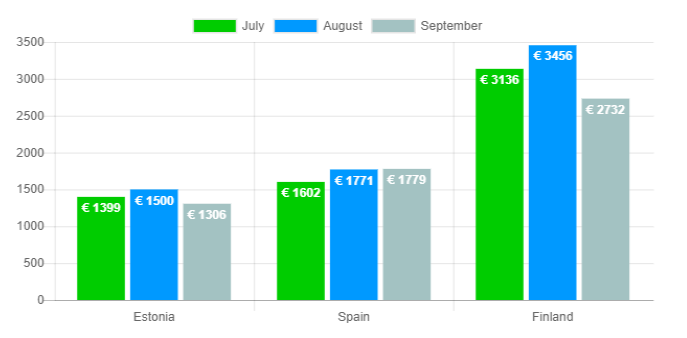

In September 2018, the average net income increased marginally in Spain but decreased In Estonia and Finland. In Estonia this was -13.8% (-€209), in Spain +0.6% (-€11) and Finland -21.4% (-€745). The total number of loans decreased in September to 1,978, slightly lower compared to the previous month (2,015).

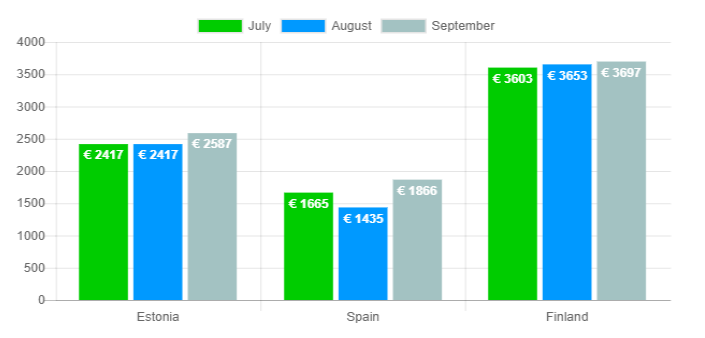

In September, the average loan amount increased across the board – specifically in Estonia +7% (+€169), Spain +30% (+€431) and Finland +1.2% (+€44).

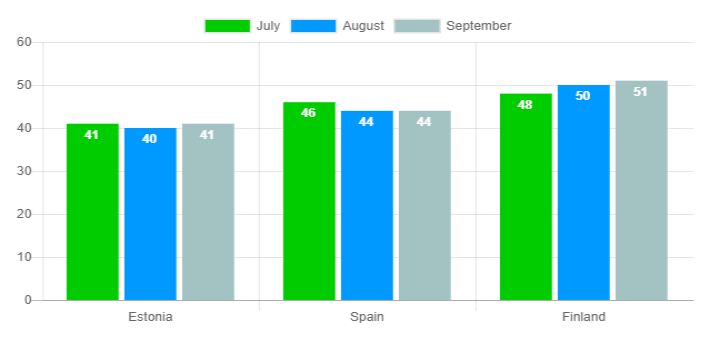

Whilst the figures haven’t changed a lot, the largest difference seen in September was the average age of Finnish borrowers raising to 51 for the first time this year. Overall, we commonly see the figures fall within the early to late 40’s range.

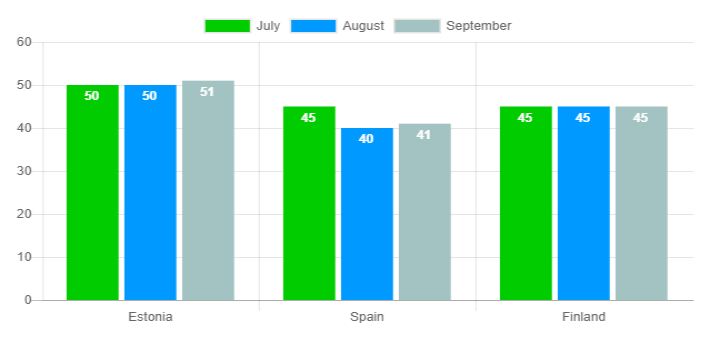

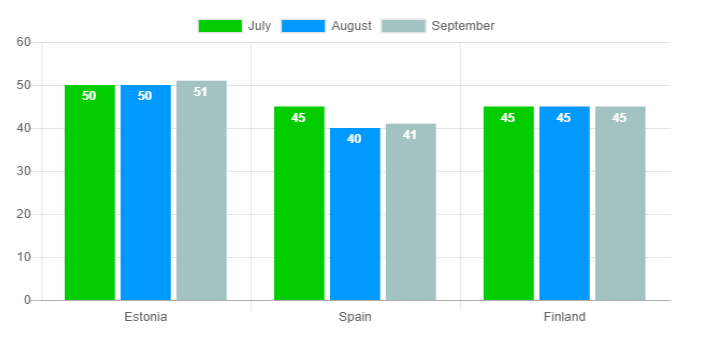

The average loan duration in September was 51 months in Estonia, 45 months in Finland and 41 months in Spain. For a more representative indicator, take a look at the most common durations below.

Loan and employment duration

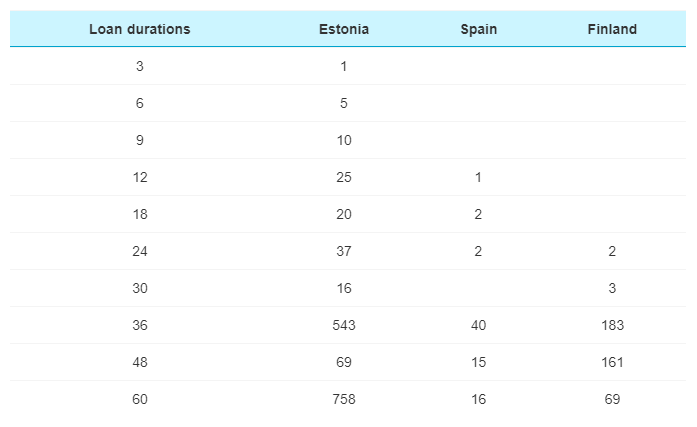

Traditionally, Bondora hasn’t focused on issuing short term loans and this is still clearly visible from the most recent data. Only 16 loans in total were issued under a duration of 12 months and were all originated in Estonia. The majority of loans issued had a duration of 36 months or above and only a total of 124 loans (6.3% of the total share) were issued with a smaller duration than this. More specifically, the most common loan duration across all countries was 60 months (843 pcs), followed by 36 months (766 pcs) and 48 months (245 pcs).

Offering the option to take a P2P loan with a duration of up to 60 months allows borrowers to have affordable monthly payments that they can budget for, along with their other commitments.

Employment duration remains the same as previous months, with ‘More than 5 years’ (815) being the most common followed by ‘Up to 5 years’ (599) and ‘Up to 1 year’ (377). This suggests that those who are confident in the stability of their employment (and ultimately their monthly income) are most likely to apply for a loan.

Education and home ownership

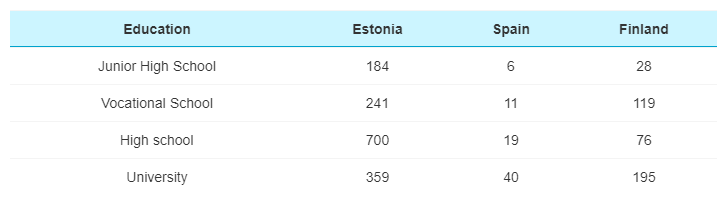

Similarly to previous months, the most common type of education declared by borrowers is of a High School standard, followed by University, Vocational School and Junior High School. Per country, the figures tell a different story. In Estonia the most common is still High School (700 pcs), whereas University is the most common Spain (40 pcs) and Finland (195 pcs).

Whilst education curriculums and institutions also vary by country and district, it provides an interesting observation when compared with other data points.

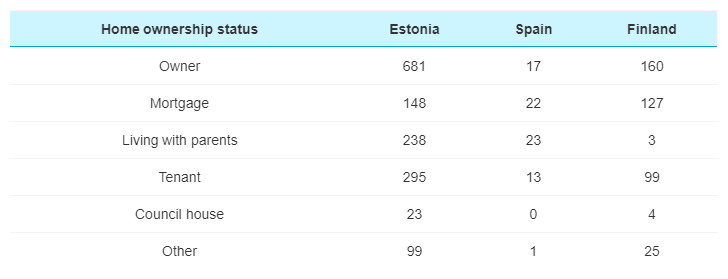

The most common home ownership status in Estonia and Finland is ‘Owner’. In Spain, the most common is ‘Living with parents’. While the status remains the same in Estonia and Finland, it fluctuates in Spain since the distribution is much more evenly spread other than ‘Council House’ and ‘Other’.

Home ownership status can give us an insight in to the cultural differences between different geographies and how this can influence the wider economy. For example, in Finland only 3 borrowers were registered as ‘Living with parents’. In Estonia, nearly half of all borrowers are homeowners.

Verification

The data below shows how many customer’s income and expenses have been verified. Regardless of whether the borrower’s income has been verified, the background checks with population and credit referencing agencies are still conducted along with a wide range of other data points used to assess their expected default rate for the P2P loan.

Overall, the total number of customers classed as verified are lower than those classed as unverified.

Which data point is the most important?

The individual risk of issuing a P2P loan to a borrower is calculated using all of the parameters above and many more. The self-reported data which is displayed to investors is typically not very predictive and has relatively little influence on the Bondora rating of a particular loan. Therefore, this information should not be viewed as the only data used in determining the expected default rate of a loan.

Overall, this post can give you a great idea of the basic profile of our borrowers and how this changes with the origination of loans in the coming months. Leave us a comment below and let us know which data points you think are the most influential in credit scoring.