IN SHORT

- We have implemented a more aggressive strategy to deal with overdue loans. One of the key strengths of this new process is that we will hand over the overdue loan to a local debt collection agency (DCA) already after a week after missing a payment. This will deliver quicker results and improve payment behavior.

- We have professional debt collection agencies and legal partners in every country where we operate (in Estonia, Finland, Spain) and they are experienced in tracking down the debtor and reaching an agreement with them.

- The DCAs that we continue working with have proven to be effective.

When CEO of Bondora, Pärtel Tomberg was invited to speak at Investeerimisraadio’s podcast in January this year, he also spoke about Bondora’s plans for 2016. Among others was this goal: “This year we want to improve the loans quality in all our markets. We strive for a more secured but faster loan processing and take steps towards a more aggressive debt collection process.”

A more aggressive collection strategy

We set out to improve our collection process and proceed with a more aggressive approach. The new process consists of three stages, it is largely automated, used across all markets where we operate and is continued until the full overdue amount is covered or the claim is written-off. Our aim is to prevent customers from defaulting on their debt obligations. We work towards reducing roll-rate between stages and increasing recovery rate in Spain and Finland.

Fast and efficient recovery process

STAGE 1 – COLLECTION

Collection without legal litigation

We start this stage with sending out in-house emails and text messages with payment details and use automated phone calls to find a solution. If the above has not been successful, we hand over the claim to a local debt collection agency (DCA) who takes over the communication with the goal to collect the debt and agree on a new payment schedule with the debtor. During this time we also forward the debtor’s information to the official debt registry. The overdue loan stays with the first DCA until the loan defaults. If the first DCA was not successful on agreeing on a new schedule and receiving at least one payment from the debtor, the claim is handed over to a second DCA. The second DCA will have 90 days to activate the debtor before we pass the case to the next stage.

STAGE 2 – RECOVERY

Legal litigation started

In case the DCAs have not been successful without using legal litigation then a court case will be filed with a local court unless for some reason the case has to be written off (read below). Court process length is dependent on the country and the local court. The case is handed over to a local bailiff after a court makes a decision. The speed of recovery will thereafter depend on the income/assets of the debtor and their other debts. During the stages the debtor has the possibility to file for debt restructuring where the court creates a payments plan for the debtor and the debtor is required to pay according to the new schedule.

STAGE 3 – WRITE-OFF

Claims unlikely to be paid back

Under the stage 3 we mark all the claims that are unlikely to be paid back. In most cases this stage consist of cases where the debtor has filed for bankruptcy, has deceased or the debtor or related claim is under criminal investigation. This stage also covers cases where the borrower has repaid the entire amount required under a settlement but it’s not enough to cover the full claim amount that we have calculated. This difference is caused by reduction of the claim or costs associated with recovery that are not reflected in the system. We are continuing to improve our system to make all recovery information available to investors.

Bankruptcy process is only initiated if bailiff has not been able to collect the debt after freezing the debtor’s assets and accounts or if the debtor itself has filed for bankruptcy. In general personal bankruptcy is not common in continental Europe as getting out of debt will take up to 7 years depending on the country.

We are on the right track

So far our collection & recovery process has proven itself, even though kicking it off properly has taken some time. After we started using the DCA services in June 2015 our investors have received over 1 million euro. Combining our new, more aggressive collection and legal litigation with the previous process will further improve our recovery performance across all markets.

Hi. Better collection is always nice. There is nice bundle of questions asked in facebook group. I like to ask 2 personal questions:

1. Who will pay DCA for pre-default collection. I do not like to do that.

2. We are losing transparency now? We cannot see stages of recovery, all is mixed now into new_stage_1?

Thanks for reply!

It is normal that overdue loans are a week late and then start paying again. It makes no sense to share their payments with DCAs unless it is not your own money. Would you do that with your own money? Probably not.

Think of it: between 8 and 35% of all payments from overdue (and defaulted) loans go to DCAs. This is just madness.

This week we launched a number of improvements to our product. I want to give some additional information a few updates that have not been fully explained earlier in the blog:

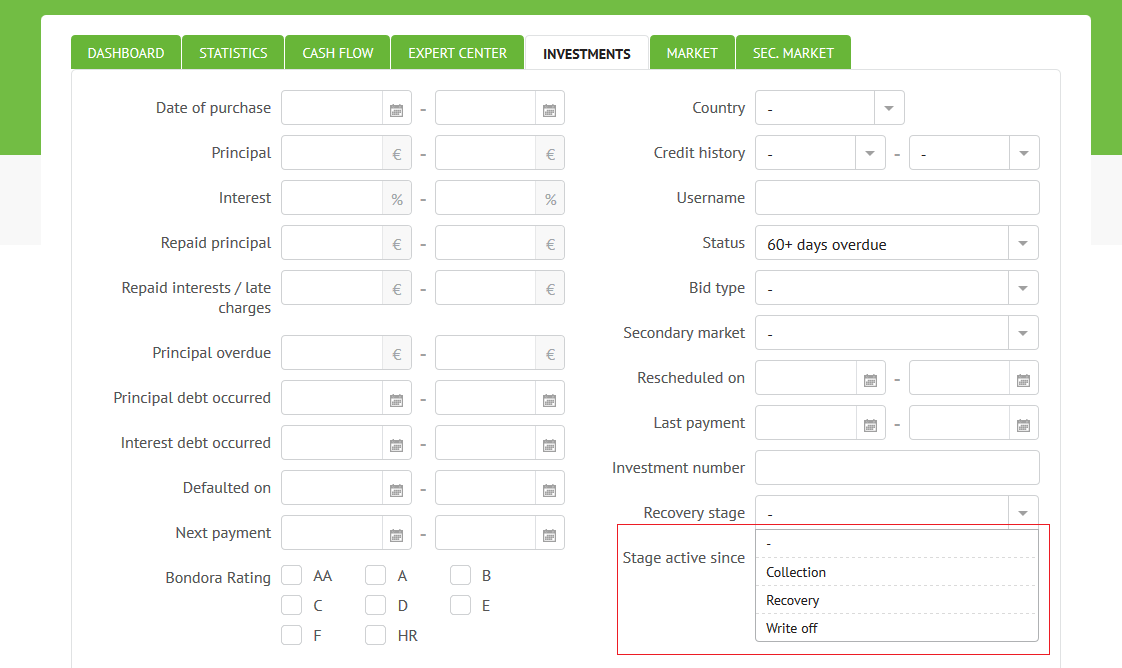

1) New collection and recovery statuses for easier filtering

2) Earlier collection and recovery efforts to reduce defaults

3) No withdrawal fees to reduce investor costs

4) New data points in the cash flow report for better transparency

5) Keeping cash flow report header frozen when scrolling for improved user experience

New collection and recovery statuses for easier filtering

Investor portfolio report and secondary market report have been updated to help quickly understand the actions taken to collect debt on an overdue loans. The filters reflect our collection and recovery process that has been developed and improved over the past years. There are three main stages: collection, recovery and write-off. These statuses are assigned based on a number of sub-stages that are visible under loan collection and recovery log. The sub-stages will evolve along with our process. Collection has 6 (in-house collection, DCA 1, DCA 2, DCA 3, cure period, loan defaulted), recovery 3 (court, bailiff, debt restructuring) and write-off 4 (deceased, bankruptcy, criminal case and write-off) sub-stages. Please note that the last active stage is assigned and kept linked with the loan even in case the loan recovers or is repaid so investors could track which actions have been taken. In case a loan is not overdue or is repaid then the latest status is useful to understand previous actions taken not what is currently happening. The full process is explained above.

Earlier collection and recovery efforts to reduce defaults

We decided to accelerate the collection efforts as our data showed that the probability of a borrower defaulting within a year increased to more than 58% in case a borrower loan becomes more than 7 days past due. Professional debt collection agencies collect a fee only when funds are recovered and these fees on average have amounted to 15% of the cash collected. Therefore if successful the collection costs on an average loan of 2500 euro loan with 80 euro monthly payment will be 12 euro (8 cents per investor on average as there are 150 investors per loan on average) in order to avoid a default of up to 1450 euro (58% of 2500 euro). Even though earlier action might be excessive for up to 42% of the cases it is overall necessary and economic to act early to decrease later defaults.

No withdrawal fees to reduce investor costs

This week we abolished the 38 cent fee on withdrawals to further increase investor costs and improve returns. This change will especially benefit smaller investors who need to withdraw smaller amounts.

New data points in the cash flow report for better transparency

We added “Total repaid from loans in default” and “Total repaid from current loans” columns to the cash flow report so it would be easier to evaluate recovery performance. You can add these new data points through the cash flow report configuration settings.

Keeping cash flow report header frozen when scrolling for improved user experience

Cash flow was further improved to keep the header row frozen when scrolling within the report. This way investors can better interact with longer time series of data.

This new process might be worth for spanish loans, since most of them have a hard time paying back.

Although I don’t think that for AA loans sending them to the DCAs after a 7 day delay will achieve anything but giving them an easy profit. I don’t know what sort of analysis you did, but I would like to see some numbers if possible.

My first guess is that sending loans to the DCAs after 7 days is too early for the highest ratings, but I haven’t done any proper analysis.

@Hélder

Taking early action will allow us to better understand the most meaningful process post-default because customers simply discard your communication if you haven’t taken additional action. This means that legal litigation can already be started post-default in cases where additional DCA action is not expected to establish a stable cash flow.

I’ll link here the “Cost-Benefit of Early Intervention” analysis made by Pärtel.

https://docs.google.com/spreadsheets/d/11hH4HGdBBrZm_nsnenJ6VUeAHAnY1uK5XOyYhqBzqgQ/edit#gid=704027990

Our data shows that the probability of a borrower defaulting within a year increased to more than 58% in case a borrower loan becomes more than 7 days past due (58% in Estonia, 66% in Finland and 87% in Spain). Therefore it’s clear that delinquencies that last for more than 7 days are not accidental and purely internal collection processes are not sufficient to mitigate default.

This idea is propably from DCAs.

There isn’t much money earned from processing loans that doesn’t recover.

But lots of to be earned from those who have habbit delaying payments.

But in overall, if overdue loan volumes go up, then maybe the cost for recovery will drop.

I wondered why DCA-s would like to process all the defaulted Bondora loans, from where there are nothing to recover. Now we know..

@Mart

This more aggressive collection strategy is Bondora’s initiative. We believe that taking early action helps to prevent customers from defaulting on their debt obligations. Regarding the question why the DCA-s process all the defaulted loans is that it’s a standard procedure and risk that comes with this kind of business.

Are you serious in sharing that excel file?

So you say there you have an process improvement of 21% for estonian loans.

Bellow you have “Default in 360D if loan 7D past due”of 58%.

Both these values are inputs in the respective cells, but what surprises me is that the “Default in 360D if loan 7D past due w collection” is defined by 58% and the “Process improvement”.

I thought the improvement was calculated based on a comparison, and not used as input to get the numbers you want. The way I see it, the numbers look very artificial and manufactured.

In short, how do you get to the 48% for estonian “Default in 360D if loan 7D past due w collection”???

@Hélder

The model shows results based on two logic: 1) cost of early collection is applied only to the loans that were ‘saved’ and 2) cost of early collection was applied to everything. I hope this makes it more clear why it makes sense to collect early. The break-even point is relatively low as the cost of collection is applied to a single monthly payment but cost of default is driven by the entire loan balance.

I understand your frustration. Our debt servicing team’s priority is to improve the collection efforts to return as much capital to the investors as possible through strong processes. After standard processes have been established then necessary reporting interfaces are built. Doing it in the different order could certainly improve transparency and reporting but not the actual performance. We are continuously looking to improve this area.

[…] muutis oma laenude taastamise protsessi, kaasates inkasso juba 7 päeva […]

You know that after slovakia and spain, investors have been very skeptical with bondora.

My suggestion is that BIG changes like this one should be announced beforehand and justified with a proper analysis.

I still remember reading here that investing in loans from slovakia would reduce risk of my portfolio. I am sure your team is full of good intentions, but I still know very little about how you got the data to make this major change.

Please don’t take this post as someone being annoying and distrustful, but instead listen to investors. We don’t ask for much, just that you justify your choices with a good analysis, and that you let us know beforehand, not a few weeks after changes are put in place.