Diversification. It’s a word you’ve probably heard many times before, but do you know what it means? Or why it’s important to your investments? Here’s a breakdown of diversification and why your investments need it and why you should want it.

Investing is great. No really, think about it. You put your money to work, it grows, you reinvest it, it grows some more. It really is brilliant. But what happens when one of your investments goes wrong?

We have two scenarios here. If you invested in only one or a few assets, anything that goes wrong with each one of them, might have a great impact on your portfolio. When they crash, you crash. But, in the second scenario, a downward performing asset will only take a minor hit on your portfolio, and that’s because you’ve diversified.

But what exactly is diversification?

Diversification in investments means you invest in multiple assets from different industries with various risk ratings and characteristics. You do this with the aim to be less impacted by any asset meltdown. In other words, you try and lower your exposure to risk.

So, if your big tech stock goes down badly, you still have other shares in the food and energy industries that are performing well, for example. If your purchased real estate suddenly loses value, your overall portfolio still has a safety net because you invested with crowdlending and commodities as well.

Put a variety of different fruits in your basket, so if one of them tastes bad, you’ve got several others to enjoy. That’s the basic idea behind diversification.

On average, it’s expected that well-diversified portfolios will generate higher long-term returns with lower risks to the investor. And who doesn’t want that?

Diversifying with Bondora

If you’re looking for a simple way to invest, (let’s be honest, who isn’t?) Bondora is the way to go. But besides being an easy-to-use investment platform, we also have multiple tools to help you diversify your portfolio.

With our most loved product, Go & Grow, you are investing in a product backed by more than 109 000 different loan claims of different risk ratings, origination countries, interest rates, loan durations, borrower profiles, etc. You can take a more in-depth look into the Go & Grow portfolio distribution here.

In short, diversification helps us to achieve an overall performance of more than 10% within Go & Grow, and this is what allows us to offer investors an expected return rate of up to 6.75%* per year. Additionally, it acts as a separate fund, which helps to make sure that Go & Grow still pays out the target return, even in difficult times, like it did during the corona crisis.

Learn more about the Go & Grow reserves in this video:

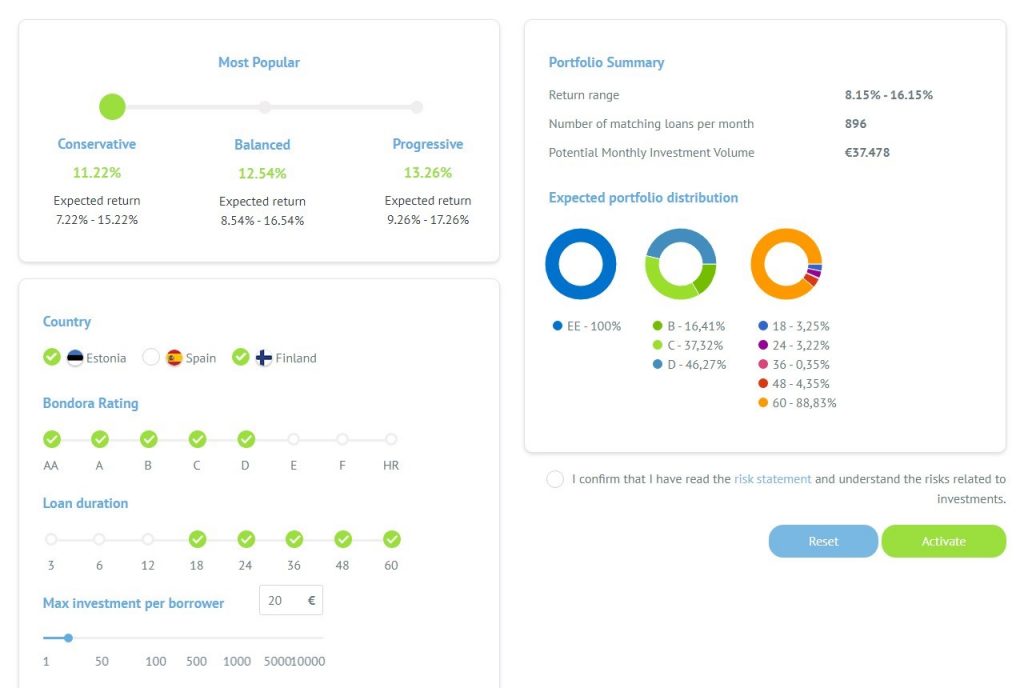

Portfolio Manager enables you to choose among different risk profiles, which lets you see the expected resulting portfolio and the loan distribution. Basically, you choose if your automatic investments will be done to the riskier side or if you’ll play a safer hand. Just slide the risk-slider until you reach a point that you feel works for you.

Portfolio Pro, on the other hand, lets you take full control of your Bondora portfolio diversification. Choose the countries, risk ratings, loan durations and interest rates that best suit you and let Bondora do the rest. What’s also great about Portfolio Pro is that it allows you to choose the maximum investment per borrower, so you can set small investment amounts, if you wish, and maximize diversification among hundreds or potentially thousands of different loan pieces.

How much diversification is enough?

This topic has been studied for decades and no one has reached a final conclusion. But there are a few strategies that could give you some initial guidance.

A common rule of thumb is subtracting your age from 100 and allocating the resultant percentage in a riskier asset, while the rest should go into less risky ones.

So if you are a young student fresh from college, for example:

100 – 22 = 78 → 78% of your portfolio in riskier assets, 22% in less risky

And if you are counting the days to your retirement:

100 – 60 = 40 → 40% of your portfolio in riskier assets, 60% in less risky

As you get older, you should rebalance your portfolio and gradually switch from a risk-taker profile to one that will make you worry less and enjoy life more. But stay vigilant: This strategy could dry up liquidity on your portfolio, so adjust it according to your preferences.

Make sure to rebalance

While diversification is great, it’s not a one-off task. Ideally, investors should track their portfolio and rebalance whenever necessary, ditching investments that are not performing and adding others that you think will deliver.

Could diversification be bad for you?

Some argue that diversification can actually hinder your portfolio’s performance. And that’s understandable. Risk and return go hand-in-hand. If you have no exposure to risk, you will also be lowering your potential for returns.

So, perhaps you aren’t that afraid of taking higher risk and you put more of your chips into one asset. Or you might choose a few less risky options, and that’s OK. But make sure your portfolio does not rely only on only one or two assets, otherwise you will be inviting the risk monster into your portfolio.

On the other end of the scale, you have the potential issue of having too many assets to sell or cash out whenever you need the money or see a potential crisis coming. Transaction fees, different platforms and brokers with different methods and requirements to get the money out, could pile up quickly. For most investors this won’t be a problem, but if you have investments with 30 or 40 different investment platforms, they might build-up and cost you a lot of your portfolio when you’re trying to walk away with your funds.

Some people also debate that during a severe economic recession many assets can spiral down at the same time, and so diversification wouldn’t save you from losing a big chunk of your portfolio. However, we just went through an economic crisis (or rather, are in the middle of it) and here’s what we’ve seen: Some assets, like stocks, crashed and got back up rather quickly. Others made a gradual comeback, like gold, and some remained stable up to now, like Bondora’s Go & Grow.

The bottom line is: Diversification can help reduce your exposure to risk. How much you want to diversify, is up to you. Do your own research, invest in what you feel comfortable with and understand, and pick the options that are a better fit for your investment profile. That way, you can always be in control of your portfolio.